The Key to the Indian EV Market

Last week, we went over how the Indian automotive industry could change post the COVID19 pandemic. If you might have missed out on it, do give it a read here. As for this week, we will discuss the opportunities concerning e-mobility in India.

It is very likely that post the coronavirus pandemic, the industry as well as the consumers will have the opportunity to move towards smart, sustainable, and clean mobility. Naturally, this will have a positive impact on the growing e-mobility trend in India. According to experts at the ETAuto Virtual Roundtable on ‘Post Covid-19: Future of Electric Vehicles Global and India’, the EV market is set to recover quickly from the coronavirus impact as compared to their fuel combustion counterparts. As a result, it is expected that the EV outlook in the medium term shall remain robust.

Experts expect EV growth

Sohinder Gill, Director General, Society of Manufacturers of Electric Vehicles (SMEV) is of the opinion that the EV industry is taking shape and that despite the coronavirus outbreak, the financial year 2020-21 is going to be a defining year for all EV segments. Naturally, the EV industry is going to be affected just like any other automotive business, but Gill states that cleaner air due to reduction in pollution is leaving a permanent impression in the minds of customers, which will promote the move towards e-mobility.

According to Sarwant Singh, Managing Partner – Middle East, Africa and South Asia, Frost & Sullivan, around 15% of the vehicles in the two-wheeler industry could be electrified in the smaller segment, especially the one below 100cc. He also feels that e-rickshaws have a good business case. These sentiments are echoed by Sulajja Motwani, Founder and CEO of Kinetic Green Energy. She feels that the outlook for two-wheelers, three-wheelers and buses remains very strong in a vast market like India. She also expects that the electrification of scooters will be faster than that of motorcycles. Additionally, she asserts that the three-wheeler market shall recover the fastest and that she expects approximately 30-40% of three-wheelers in India to be electric in next 8 years, especially with the low transportation cost, e-commerce delivery coming in as well as the need for last-mile connectivity solutions.

According to Sarwant Singh, Managing Partner – Middle East, Africa and South Asia, Frost & Sullivan, around 15% of the vehicles in the two-wheeler industry could be electrified in the smaller segment, especially the one below 100cc. He also feels that e-rickshaws have a good business case. These sentiments are echoed by Sulajja Motwani, Founder and CEO of Kinetic Green Energy. She feels that the outlook for two-wheelers, three-wheelers and buses remains very strong in a vast market like India. She also expects that the electrification of scooters will be faster than that of motorcycles. Additionally, she asserts that the three-wheeler market shall recover the fastest and that she expects approximately 30-40% of three-wheelers in India to be electric in next 8 years, especially with the low transportation cost, e-commerce delivery coming in as well as the need for last-mile connectivity solutions.

Thinking Big – Government’s Vision

With industry expected to grow four-fold, the Indian government has identified the huge EV potential and as a result, are targeting 30% EV penetration by 2030. The government is focusing on city buses, 3 wheelers and passenger cars for shared mobility in the current phase. They expect that the electric two-wheeler market will leapfrog on its own business case in India. The government’s vision and targets are as follows:

- 2023: All three-wheelers sold in India to be only electric

- 2025: All two-wheelers below 150cc sold in India to be only electric

- 2026: All new cars sold for commercial use (Uber, Ola etc.) to be only electric

- 2030: All inter-city public transport to be 100% electric including buses, three-wheelers, taxi fleets

The Indian government targets to make India one of the largest EV production hubs in the world and has sanctioned USD 1.4 billion to support this over 3 years. Under the scheme FAME-II, the government is now incentivising vehicles based on battery size and in terms of volume and plans to incentivise about 7000 electric buses (priced up to USD 278,000), 20,000 hybrid passenger cars (priced up to USD 20,800), 35,000 electric passenger cars, 500,000 electric three-wheelers (priced up to USD 7,000) and 1,000,000 electric two-wheelers (priced up to USD 2,000). Furthermore, the government also plans to have 2700 charging stations in major metros in 3 years and is providing USD 140 million for setting up charging infrastructure.

The Indian government targets to make India one of the largest EV production hubs in the world and has sanctioned USD 1.4 billion to support this over 3 years. Under the scheme FAME-II, the government is now incentivising vehicles based on battery size and in terms of volume and plans to incentivise about 7000 electric buses (priced up to USD 278,000), 20,000 hybrid passenger cars (priced up to USD 20,800), 35,000 electric passenger cars, 500,000 electric three-wheelers (priced up to USD 7,000) and 1,000,000 electric two-wheelers (priced up to USD 2,000). Furthermore, the government also plans to have 2700 charging stations in major metros in 3 years and is providing USD 140 million for setting up charging infrastructure.

Roadblocks for the EV Industry

Electrification is not bound to be all smooth sailing and one can expect some roadblocks along the way. Firstly, the EV supply chain in India is not strong, because very few suppliers are present and most of electronic components required in electric vehicles are imported from China. Especially after the coronavirus outbreak, where businesses are going to be wary of their dependence on China, a strong and diversified supply chain is the need of the hour. This presents an excellent opportunity for EV-related suppliers from other countries to stake a claim in the Indian EV-market pie. Another major roadblock for the Indian EV industry is that the industry is largely driven by cost. The cost of the battery packs is approximately 50% of the total cost of the electric vehicle. The battery packs are assembled locally, however, cells and many battery pack components are not produced locally. Suppliers from locations other than China, with right solutions for the vast yet cost sensitive Indian market will have an excellent market.

Furthermore, electric vehicles are currently not mainstream in India due to factors such as safety and range. Battery packs generate a lot of heat, and if this heat is not adequately and properly dissipated to the surroundings, the batteries and in turn, the vehicle run a huge risk of catching fire, which makes fire anxiety an extremely legitimate safety concern. It is necessary to prevent the phenomenon of thermal runaway, where adjacent cells rapidly catch fire to spread over the entire battery pack once a single cell gets ignited. Another important concern that customers have is the range of electric vehicles. Owing to the lack of adequate charging infrastructure in the country, the population is anxious about the batteries running out of power, leaving them stranded with nowhere to go. Electric vehicles, as a result, are seen as unfit for long distance journeys. This fast-growing E-mobility market needs suppliers with cost effective technologies for range extensions.

Furthermore, electric vehicles are currently not mainstream in India due to factors such as safety and range. Battery packs generate a lot of heat, and if this heat is not adequately and properly dissipated to the surroundings, the batteries and in turn, the vehicle run a huge risk of catching fire, which makes fire anxiety an extremely legitimate safety concern. It is necessary to prevent the phenomenon of thermal runaway, where adjacent cells rapidly catch fire to spread over the entire battery pack once a single cell gets ignited. Another important concern that customers have is the range of electric vehicles. Owing to the lack of adequate charging infrastructure in the country, the population is anxious about the batteries running out of power, leaving them stranded with nowhere to go. Electric vehicles, as a result, are seen as unfit for long distance journeys. This fast-growing E-mobility market needs suppliers with cost effective technologies for range extensions.

Suppliers in demand!

According to a report from ReportLinker, the global electric vehicle and electric vehicle infrastructure market is projected to reach 4.18 million units by 2021 from an estimated 3.42 million units in 2020, at a CAGR of 22.1%. India is expected to be a significant contributor to this growth. As per the data by Society of Manufacturers of Electric Vehicles (SMEV), the Indian EV industry recorded a 20% increase in domestic sales. This 20% growth has largely come from two-wheelers. However, in the latter part of the year, the electric cars in the premium segment seemed to gain acceptance which indicates a positive upturn for a much higher volume of sales in FY2021. According to figures provided by P&S Intelligence in an abstract of their latest report on the Indian electric bus market, the electric bus market in India is foreseen to reach over 7,000 units by 2025 with a CAGR of 53 % in the period 2018 – 2025.

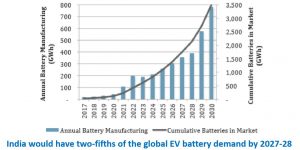

India has massive potential in the power electronics component industry, say Frost & Sullivan. They expect its EV value chain to reach USD 4.8 billion in 2025. Approximately 61% of the power electronics market share will be dominated by the two-wheeler segment by 2025. Further, it is expected that around 33% of the EV motor market will emerge from demand in electric buses in India in 2025. Additionally, according to Rocky Mountain Institute, it is expected that India would have two-fifths of the global battery demand by 2027-28.

India has massive potential in the power electronics component industry, say Frost & Sullivan. They expect its EV value chain to reach USD 4.8 billion in 2025. Approximately 61% of the power electronics market share will be dominated by the two-wheeler segment by 2025. Further, it is expected that around 33% of the EV motor market will emerge from demand in electric buses in India in 2025. Additionally, according to Rocky Mountain Institute, it is expected that India would have two-fifths of the global battery demand by 2027-28.

Factors such as a weak and dependent supply chain, government incentives, rising growth projections and sales volumes point towards massive opportunities for foreign Tier-1, Tier-2 as well as Tier-3 suppliers to not only export to India, but also for licensing of technology such as Battery Management Systems (BMS), battery pack designs, motors and controllers. Furthermore, there is also a scope for foreign businesses to work on technology development with large Indian automotive manufacturers and government institutions.

For more details and to know more about the Indian EV Market Opportunities, please write to eashaan@quanzen.com.

{kind=link}